Financing a trailer shapes cash flow and uptime. Treat the loan like a tool.

Align the structure with your revenue pattern. Connect the asset to your main loads. Then, negotiate terms that protect you during market fluctuations.

Build a complete budget

Price the entire acquisition, not just the sticker. Add taxes, title, delivery, and the first service. Include winches, ramps, toolboxes, tie-downs, and spares. Set a down payment that lowers interest without starving working capital.

Pick a payment you can cover in slow months. Hold a reserve for fuel, insurance, and routine service.

Match the trailer to your duty cycle

Buy for the work you run most. If you live at docks with legal-height freight, a flatbed loads from any side. If you haul taller machines, a step deck lowers the main deck and improves stability. Compare units on the Inventory Page.

If you weigh a short contract, read Rent vs Buy a Heavy Haul Trailer: A Cost Comparison for Fleet Managers in the blog.

Clarify your credit picture

Pull your report and score before you apply. Fix errors and pay down small balances. Lenders reward clean histories and steady deposits.

Bring organized statements and tax returns. Strong files help you qualify for better trailer loans with lower rates.

Know the four levers in trailer loans

Most offers hinge on rate, term, down payment, and fees.

- Rate and APR. The rate drives payment size. APR shows total cost with fees. Compare APR across trailer loans to see the real gap.

- Term. Short terms raise payments and cut interest. Long terms lower payments and raise interest. Match the term to asset life.

- Down payment. More cash down often lowers the rate on trailer loans.

- Fees and add-ons. Ask about origination, doc, and processing fees. Decline extras you do not need.

Request an amortization schedule. Confirm how the lender applies extra principal.

Choose the right source for trailer loans

Pick from three common paths.

- Dealer financing. Fast decisions and simple paperwork on many trailer loans.

- Banks and credit unions. Strong rates for strong credit.

- Equipment finance firms. Flexible structures for younger businesses.

Collect at least two quotes. Compare APR, total paid, prepayment rules, and any early payoff fee. Line offers up side by side so you see which trailer loans protect cash the best.

New vs used

New units have long lives and high uptime. Used units are cheaper but need tight inspection. Verify service records.

Check hubs, brakes, wiring, lighting, and suspension parts. Uneven tire wear can signal alignment issues.

See current stock on the Inventory Page. For programs and terms, visit the Financing Page.

Align structure with cash flow

Pick a term that fits how you earn. Many heavy-duty platforms justify 48 to 72 months. Do not pick a term that outlasts the trailer.

Ask about seasonal structures if revenue swings by quarter. Keep the plan clear and straightforward.

Insure the asset before you sign

Call your agent early. You need physical damage, liability, and cargo coverage that fits your lanes and loads. If required, list the lender as loss payee. Confirm rules across states and ports.

Assemble a clean file

Bring a complete packet. Please include your ID and formation documents. Also, provide three to six months of bank statements. Include a recent tax return or year-to-date profit and loss statement.

Don’t forget an insurance binder and a purchase order or bill of sale. Clean files speed approval on trailer loans.

Spot red flags

Slow down before you sign. Watch for teaser rates that reset, harsh prepayment penalties, forced add-ons, and vague collateral terms. Ask for edits and clear payoff instructions.

Protect the payment with upkeep

Your trailer funds the loan. Keep it earning. Check tires, lights, brakes, and hubs before every trip.

Grease bearings on schedule. Clean wiring and grounds. Fix defects the day you find them.

If the platform no longer fits your core freight, upgrade instead of fighting constant repairs. See options on the Financing Page.

Practical scenarios

Flatbed fits palletized freight and frequent dock stops. Step deck fits compact equipment and taller machines. Trailer loans spread cost while you add lanes and customers.

If you still compare renting to buying, read Rent vs Buy a Heavy Haul Trailer: A Cost Comparison for Fleet Managers on the blog.

Common mistakes

Chasing the smallest payment and ignoring total interest. Delaying insurance. Accepting harsh prepayment rules. Buying the wrong platform. Forgetting title and delivery costs. Skipping used-unit inspections.

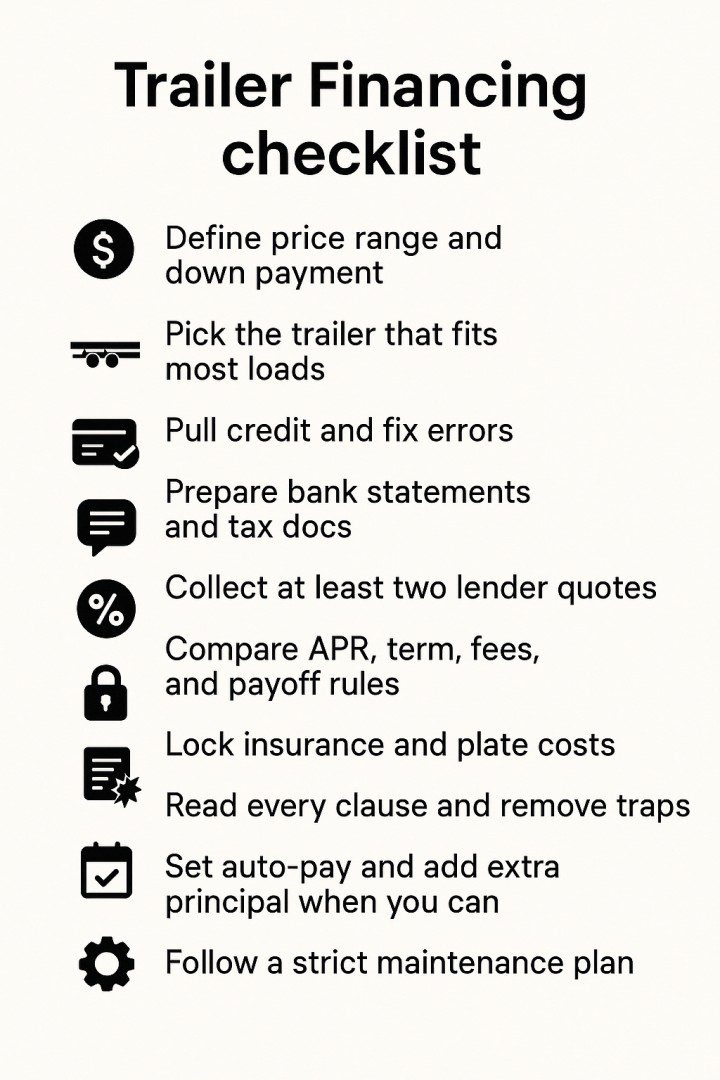

A short checklist

- Define price range and down payment.

- Pick the trailer that fits most loads.

- Pull credit and fix errors.

- Prepare bank statements and tax docs.

- Get at least two quotes on trailer loans.

- Compare APR, term, fees, and payoff rules.

- Lock insurance and plate costs.

- Read every clause and remove traps.

- Set auto-pay and add extra principal when you can.

- Follow a strict maintenance plan.

Final thought

Treat trailer financing like a strategic tool. Align the asset with your freight, align the structure with your cash flow, negotiate clear terms, and execute with discipline.

For current programs and trailer loans, visit the Financing Page. To see what sits on the lot, open the Inventory Page.